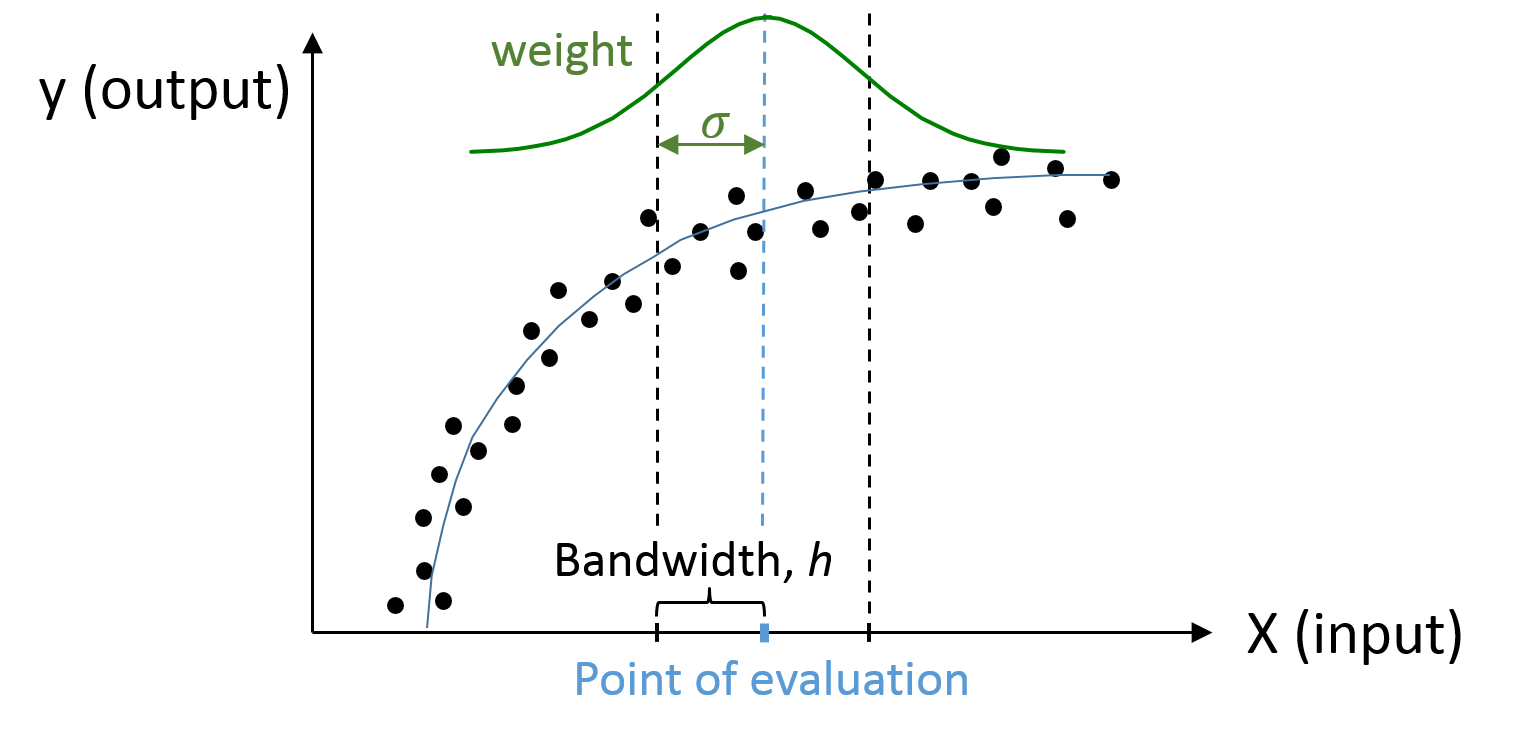

SCKLS (shape constrained kernel-weighted least squares) estimator integrates kernel-weighting to convex nonparametric least squares.

Kernel regression is one of the powerful nonparametric estimation methods. By imposing more weight to some closer points, kernel regression helps to avoid over-fitting although it requires the tuning parameter, bandwidth. By imposing some shape constraints such as monotonicity and concavity, we propose SCKLS estimator and apply it to estimate production function with simulated and real data. We also investigate the relationship with Convex Nonparametric Least Squares (CNLS) and we found that CNLS is minimum bias estimator in the class of SCKLS estimator. This is on-going research with Daisuke Yagi. This is the first chapter of his dissertation.